Table of Contents

The insurance industry has gathered steam after weathering the impacts of the hawkish move of the Fed to cut down inflation, concerns over the Russia-Ukraine conflict and a strong dollar. The industry has gained 2.5% year to date. Improved pricing, prudent underwriting, increased exposure, streamlined operations, a wider global presence and a solid capital position have helped the industry.

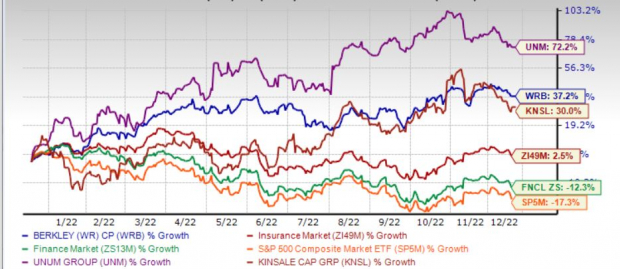

Banking on strong fundamentals and benefiting from a favorable macro backdrop, W.R. Berkley Corporation (WRB – Free Report) , Unum Group (UNM – Free Report) and Kinsale Capital Group Inc. (KNSL – Free Report) have not only outperformed the industry but have also crushed the market and the Finance sector. These companies are well-poised to sustain the bull run next year.

Image Source: Zacks Investment Research

What Helped the Insurers Sail Through This Year?

The economy has been growing slowly, as evident from the GDP that increased at an annualized rate of 2.9% in the third quarter of 2022. Per December Economic Projections of the Fed, GDP in 2022 is estimated to improve 0.5%, while the unemployment rate is expected to be 3.7%.

Despite an above-average hurricane season, continued increases in pricing, reinsurance programs and favorable reserve development helped non-life insurers sail through.

Swiss Re estimated insured losses from natural catastrophes of $35 million for the first half of 2022, while Munich Re estimated losses of $65 billion, with slightly less than half insured. Per a report published in LAW360, AM Best estimated the net income of U.S. property and casualty insurers to decline 17% year over year to $31.4 billion in the first half of 2022.

Global commercial insurance prices rose for 20 straight quarters though the magnitude slowed down over the last seven quarters, per Marsh Global Insurance Market Index.

Better pricing ensures improved premiums and prudent claims payment. Per Deloitte Insights, gross premiums are estimated to increase sixfold to $722 billion by 2030. China and North America should account for more than two-thirds of the global market, per the report. Per Willis Towers Watson’s 2021 Insurance Marketplace Realities spring update report, except for one, 26 lines should witness a price rise, while seven lines should witness a mix or flat increase.

The insurance industry is rate sensitive. The interest rate environment has started to improve. The Fed has already made six hikes in 2022, with more to come. An improving rate environment is a boon for insurers, especially long-tail non-life insurers and life insurers.

Increased awareness following the pandemic continues to support the life insurance market. However, according to LIMRA’s Second Quarter U.S. Individual Life Insurance Sales Survey, the number of policies sold decreased 9% in the first half of 2022 though the total net premium rose 11%. Concerns over inflation and a slowdown in the economy have likely weighed on the sales figures, per the report.

Nevertheless, a solid surplus level continues to aid insurers in pursuing strategic mergers and acquisitions to gain market share, expand in niche areas, and diversify operations into new business lines and geography.

The industry is undergoing accelerated digitalization. Increased use of technology like blockchain, artificial intelligence, advanced analytics, telematics, cloud computing robotic process automation, Chatbot and RoboAdvisory, and insurtech solutions continue to expedite business operations and save costs.

Can These Stocks Retain the Bull Run Next Year?

Per December Economic Projections of the Fed, GDP in 2023 is pegged to grow 0.5%, while the unemployment rate is pinned to be 4.6%. As the insurance industry is an important contributor to the country’s GDP, it is well-poised for growth, given the economic expansion.

At its December meeting, Fed predicted to take the interest rate to 5.1% in 2023 to combat its expected 3.1% inflation. Insurers, being the beneficiaries of the rising rate environment, are positioned to generate better investment results.

The improved pricing environment should continue through 2023, albeit at a slower pace. Better pricing, improved underwriting standards and streamlined operations should continue to fuel premium. Per Deloitte Insights, the life insurance premium is estimated to increase 1.9% in 2023. The report also stated that trends like commercial lines witnessing growth at a faster pace than personal lines, homeowners’ premiums improving better than personal auto are likely to continue in 2023.

Insurers should continue to invest heavily in technology to improve scale and efficiencies, while M&A should be on the rise as more insurers seek growth through expansion.

Picks for Better Return

With the help of the Zacks Stock Screener, we have selected three insurance stocks that rallied this year and are poised to retain the momentum next year. These top-ranked stocks have rallied more than 25% year to date and have an impressive track of increasing dividends. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

These stocks have delivered earnings surprises in each of the last four reported quarters and witnessed northbound estimate revisions.

Greenwich, CT-based W.R. Berkley is one of the nation’s largest commercial lines property casualty insurance providers. This Zacks Rank #2 (Buy) insurer has an impressive VGM Score of A.

Several startup units in various business lines, the expansion of the international business that offers diversification benefits, rate increase, benefits derived from market dislocations, and high retention should drive its Insurance business. WRB’s focus on commercial lines, including excess and surplus lines, admitted lines, and specialty personal lines, bodes well. Premium growth in the international unit is mainly supported by the emerging markets of the U.K., Continental Europe, South America, Canada, Scandinavia, Asia and Australia.

A strong capital position helps W.R. Berkley deploy capital via share repurchases, special dividends and dividend hikes that enhance shareholders’ value. In June 2022, W.R. Berkley approved a 15.3% hike in its quarterly dividend, marking the 17th consecutive increase since 2005. Also, the board approved a special cash dividend of 50 cents per share, marking 14 special dividends since 2012. Its dividend yield of 0.5% is higher than the industry average of 0.3%. WRB targets a return on equity of 15% over the long term.

The Zacks Consensus Estimate for W.R. Berkley’s 2023 earnings suggests 11.5% growth from the year-ago reported figure on 13% higher revenues. Expected long-term earnings growth is pegged at 9%. The consensus estimate has moved up 1.1% in the past 30 days. The company has a Growth Score of B.

Solid insurance business, strong international unit and sturdy financial position continue to drive this insurer. Shares of WRB have rallied 37.2% year to date

Richmond, VA-based Kinsale offers various insurance and reinsurance products across all 50 states of the United States, the District of Columbia, the Commonwealth of Puerto Rico and the U.S. Virgin Islands. The insurer currently sports a Zacks Rank #1.

Kinsale is well-poised to deliver improved margins and lower loss ratios, banking on intensified focus on the E&S market across the United States. The insurer targets clients with small and medium-sized accounts, which have better pricing and are less prone to competition. Kinsale estimates low-double-digit rate increases across the book of business. Kinsale remains well-poised to benefit from continued market dislocation, as it has resulted in improved submission flows and better pricing decisions.

Boasting the best combination of high-growth and low-combined ratios among its peers, KNSL targets a combined ratio in the mid-80s range over the long term.

Based on solid cash flow, KNSL has increased dividends since 2017, seeing a five-year CAGR (2016-2022) of 14.6%. For the long term, it targets maintaining an operating return on equity in the mid-teens range.

The Zacks Consensus Estimate for Kinsale’s 2023 earnings suggests 22.4% year-over-year growth on 32.2% higher revenues. The consensus estimate has moved up 0.6% in the past seven days. It has a Growth Score of B.

Focus on the excess and supply (E&S) market, prudent underwriting, lower expense ratio, growth in the investment portfolio and effective capital deployment should continue to drive KNSL. Shares of KNSL have rallied 30% year to date.

Chattanooga, TN-based Unum, which currently carries a Zacks Rank #2, provides disability insurance, long-term care insurance, life insurance, and employer and employee-paid group benefits and related services.

Unum should continue to benefit from disciplined sales trends, strong persistency in group lines, growth of new products, and favorable benefit experiences. Management is focused on moving on to a mix of businesses with higher growth and stable margins.

Riding on a solid capital position, Unum hiked dividends 13 times in the last 12 years, yielding 3.2%, higher than the industry average of 1.6%. In December 2022, Unum’s board approved a share repurchase program that authorizes it to repurchase shares up to $200 million from Jan 1, 2023, through Dec 31, 2023.

The Zacks Consensus Estimate for Unum’s 2023 earnings suggests 0.6% year-over-year growth on 2.2% higher revenues. The expected long-term earnings growth is pegged at 12.2%. UNM estimates 45-55% growth in adjusted operating EPS by 2024.

The Zacks Consensus Estimate for Unum’s 2022 earnings has moved up 0.5% in the past 30 days. UNM is well-poised for progress, evident from its impressive VGM Score of B.

Disciplined sales trends, persistency and favorable benefit experiences should continue to drive UNM. Unum’s shares have rallied 72.2% year to date.

More Stories

Ashwagandha’s Impact on Cortisol Levels in Stressed People

Health care cyberattack ‘likely one of the worst,’ expert says

Accessing Medicinal Cannabis in the UK: A Comprehensive Guide